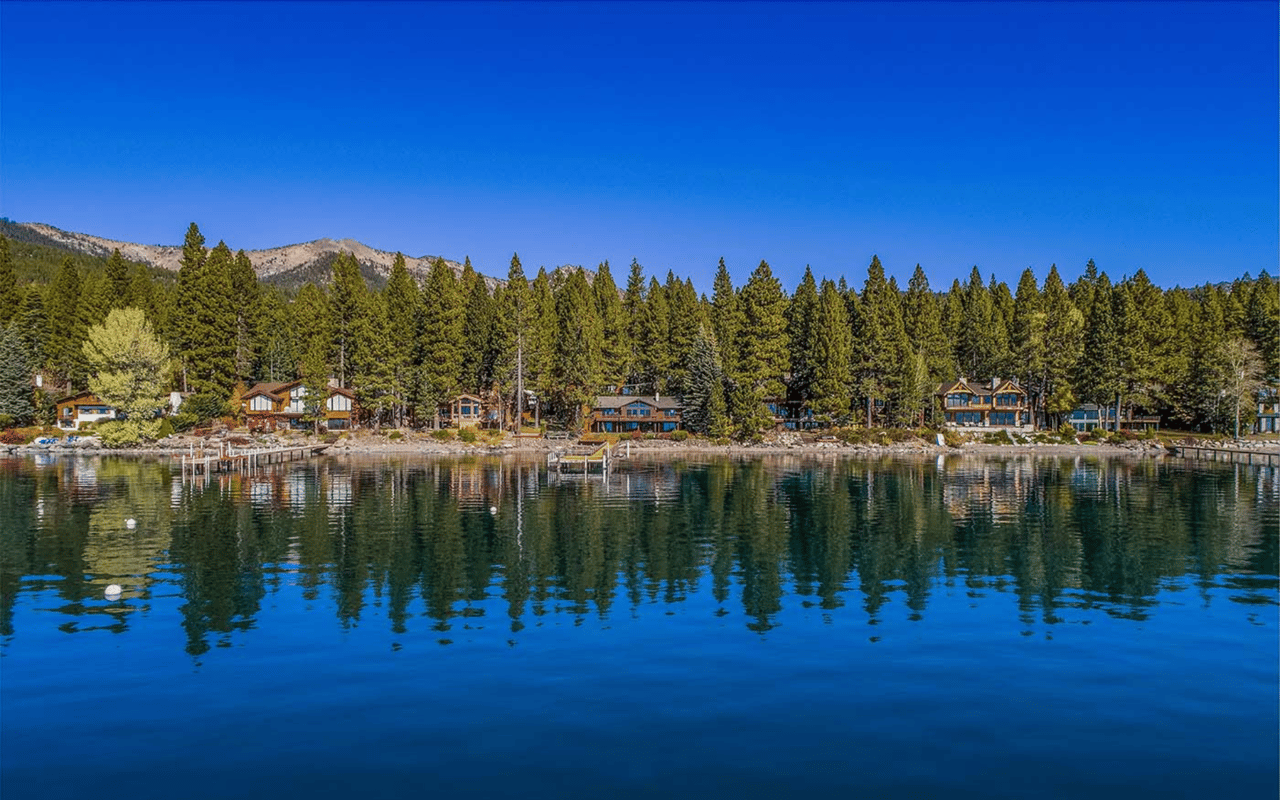

Incline Village

Year End 2022, a Narrative of Incline Village Real Estate

- Lakeshore Realty

- 01/18/23

With the number of sales and sales volume decreasing, you would expect the median price of homes to decrease as well

Read MORE

Incline Village Real Estate Market Update from our Agent Insiders

- Lakeshore Realty

- 07/21/22

Here’s what our local agents are reporting about Incline Village this July.

Read MORESorry, we couldn't find any results that match that search. Try another search.